I am here today to talk about subsequent events. A subsequent event is an event that occurs between a business's year-end date and the date that the financial statements are approved for issue. A fiscal year has a start date and a year-end date, which can last either one year or an operating cycle, whichever is longer. For this fiscal year, I chose a year ending on December 31st. It is important to note that two-thirds of all companies have a year-end date that is either December 31st or close to it. During the reporting period, which falls between the start and end dates of the fiscal year, all transactions must be reported in the financial statements. This is the basis of accrual accounting, which is required under IFRS and ASPE. The year-end date serves as the cutoff point for recognizing transactions within that fiscal period. After the year-end, several weeks or months may pass before the Board of Directors approves the financial statements for issue. During this time, the business will tasks such as counting and pricing inventory, preparing adjusting entries, ensuring the completeness of accounting records, and having the financial statements audited. This period between the cutoff date and the date of approval of the financial statements is known as the subsequent events period. During the subsequent events period, significant events that impact the company's business may occur. If these events are material, they should be reflected in the financial statements, even if they happened after the cutoff date. This information is necessary for stakeholders to predict the future and make informed decisions. However, the decision to include subsequent events in the financial statements depends on the nature of the event and when it occurred. Subsequent events can be classified into two types: adjusting events and non-adjusting events. Adjusting events occur...

Award-winning PDF software

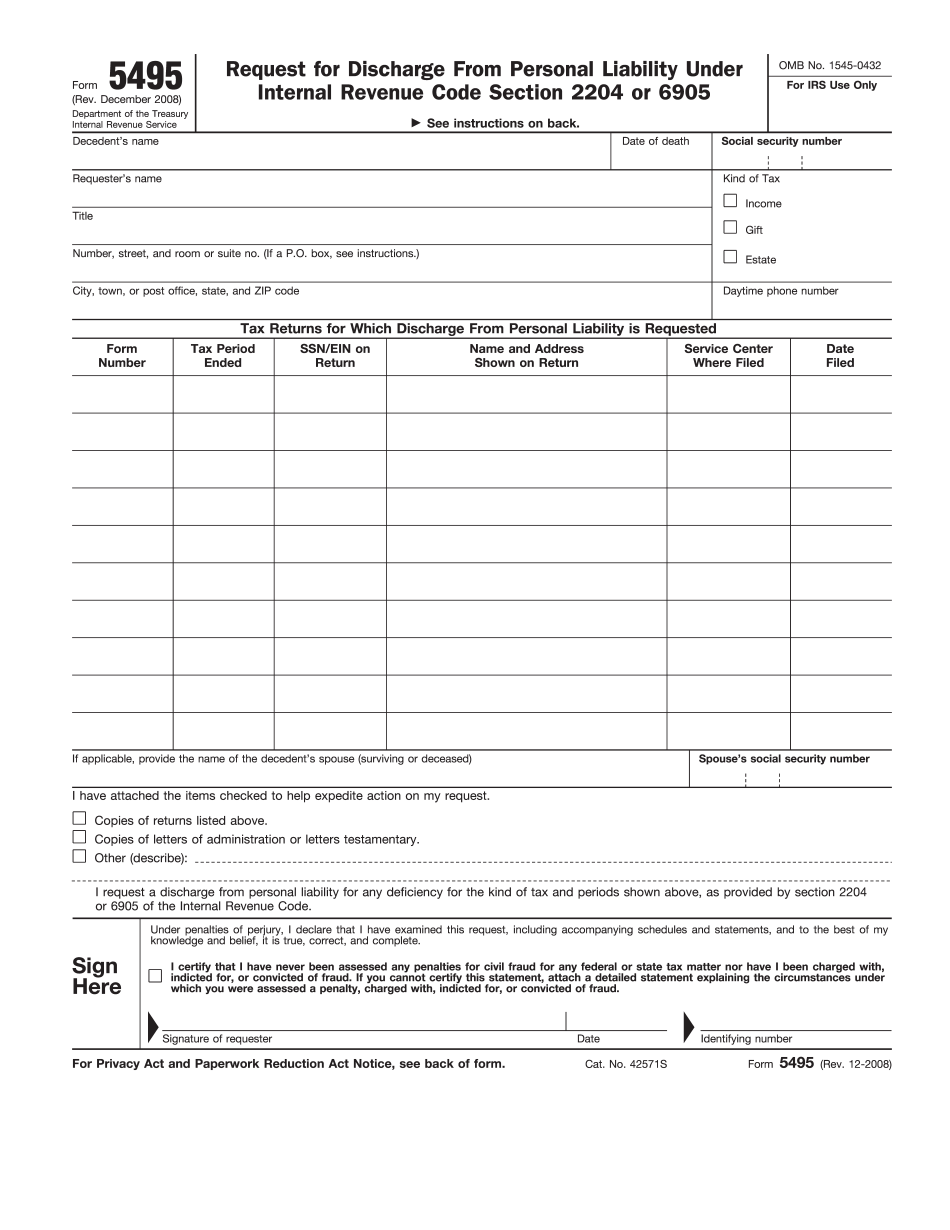

Video instructions and help with filling out and completing Which Form 5495 Subsequent