Divide this text into sentences and correct mistakes: - Everyone bill that's been here for money evolution calm in today's video. - I'm gonna be helping you to answer the question what is a fiduciary. - More specifically, I'm gonna be talking about some of the differences between a fiduciary and a financial adviser. - This is something that's obviously been getting a lot of attention here over the last couple of years, especially with the Department of Labor trying to create their definitions for a fiduciary standard. - So hopefully this video gives you some great ammunition to ask some of the right questions as you're maybe exploring some options for yourself and for your portfolios. - So first of all let's talk about a definition here. - So I went out on the internet lots of different topics and information pertaining to this. - But one definition I found on the internet said that only fiduciary advisors are legally and ethically required to put your best interest before that of their own. - Another analogy that I saw that kind of made sense to a degree was imagine you're going out to buy a new suit with a financial advisor. - The salesman is only required to sell you a suit that fits, whereas a fiduciary advisor is required to not only sell you a suit that fits but also that looks good on you. - So when you see those kinds of definitions and hear that analogy, then it might become very clear that you need to find a fiduciary financial advisor. - One of the reasons that the fiduciary has been getting a lot of attention here is what we're trying to do, I think what the industry is trying to do hopefully is to eliminate or at least reduce as many of the potential conflicts of interest...

Award-winning PDF software

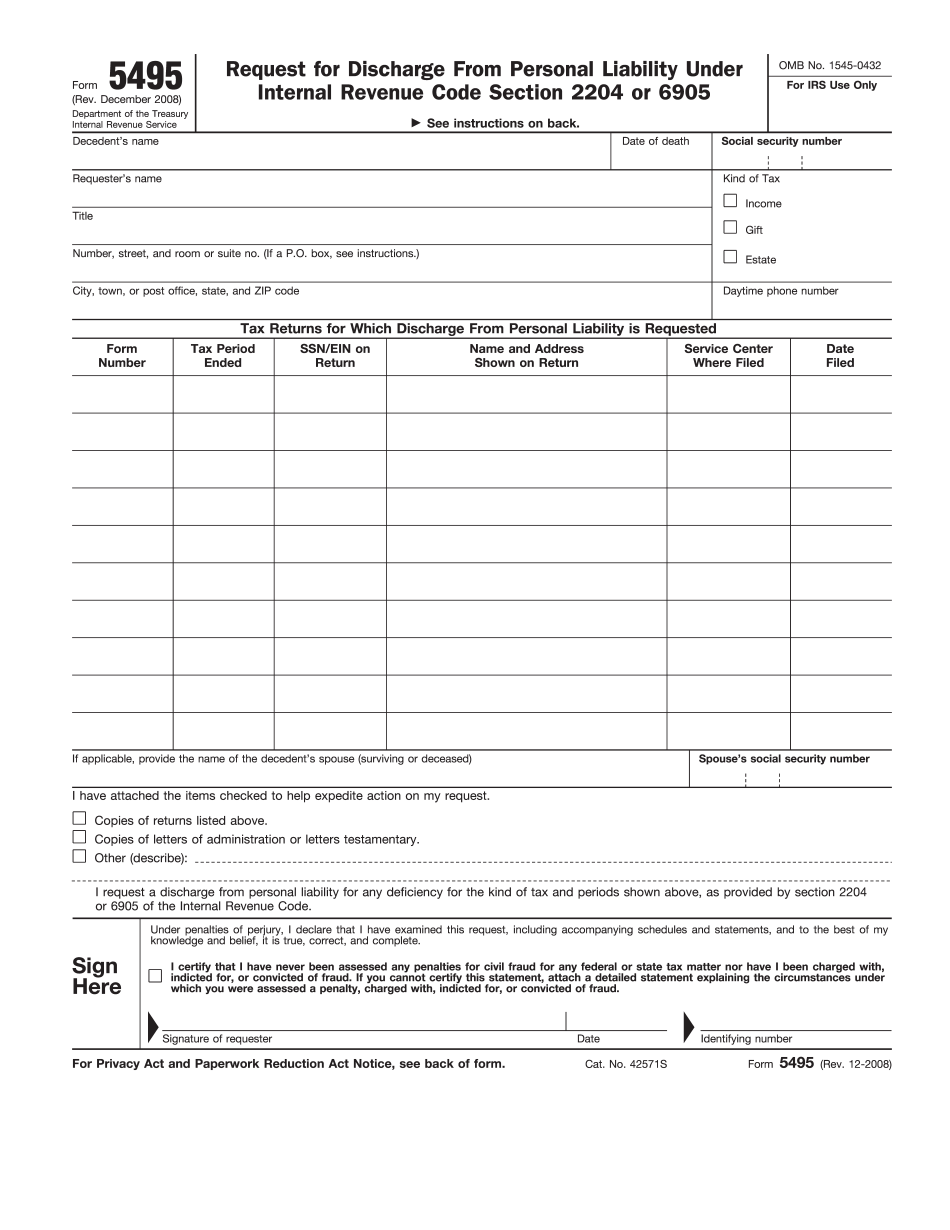

Video instructions and help with filling out and completing What Form 5495 Fiduciary