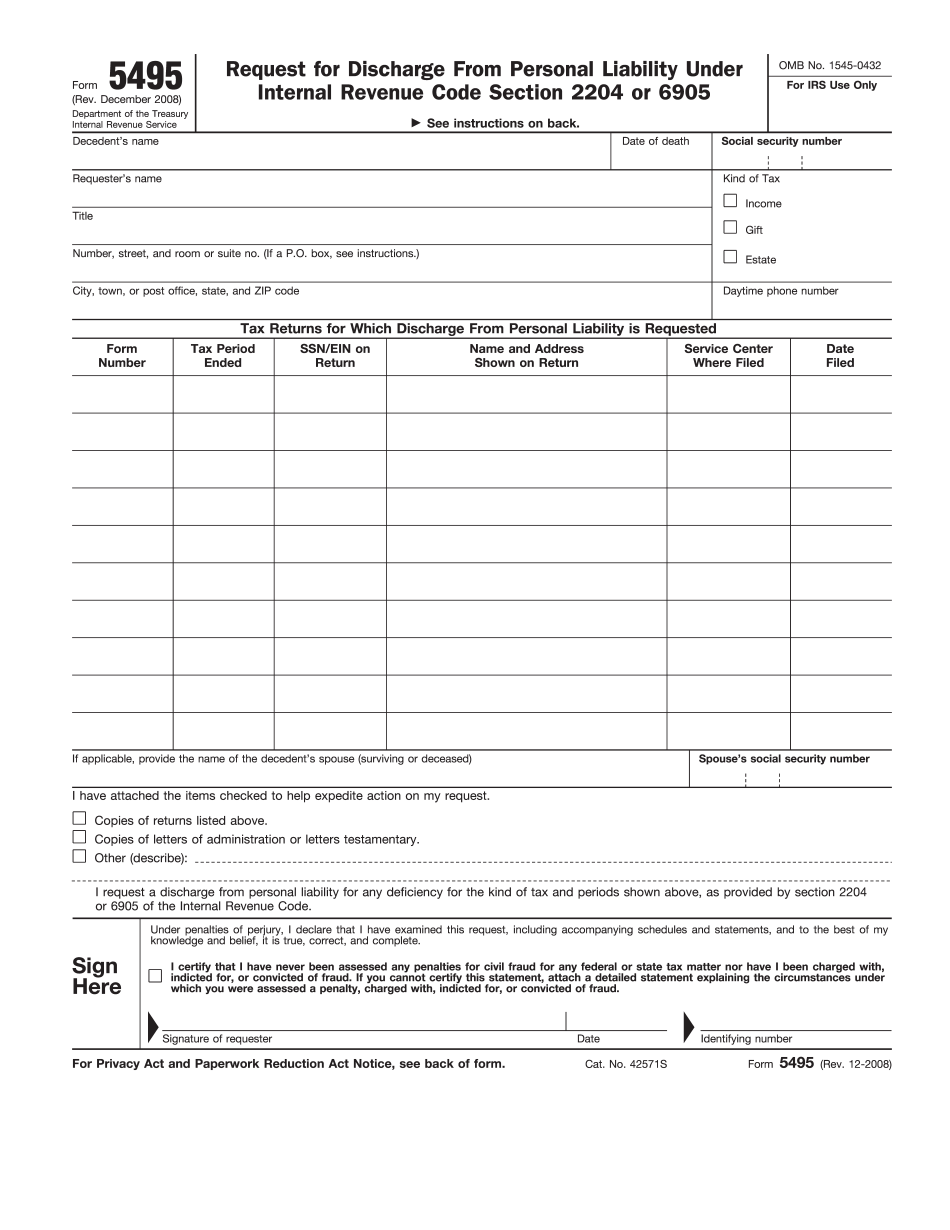

Form 5495

Home

Top Forms

Form 5495

Home

Top Forms

Get

Form 5495 Judicial 2017-2025

Get Form

Home

TOP Forms to Compete and Sign

Form 5495 Judicial

👉

Did you like how we did? Rate your experience!

Rated

4.5 out of

5

stars by our customers

561

Award-winning PDF software

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

Get Form

100%

Loading, please wait

.

.

.