Form 5495

Home

Top Forms

Form 5495

Home

Top Forms

Get

Are Form 5495 Estimated 2017-2025

Get Form

Home

TOP Forms to Compete and Sign

Are Form 5495 Estimated

👉

Did you like how we did? Rate your experience!

Rated

4.5 out of

5

stars by our customers

561

Award-winning PDF software

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

Related Content - Are Form 5495 Estimated

How to apply for the GI Bill and related benefits - Veterans Affairs

Nov 12, 2021 — How do I apply? You can apply online right now. Just answer a few questions, and we'll help you get started with the education benefits form ...Missing: 5495 - | Must include: 5495 -

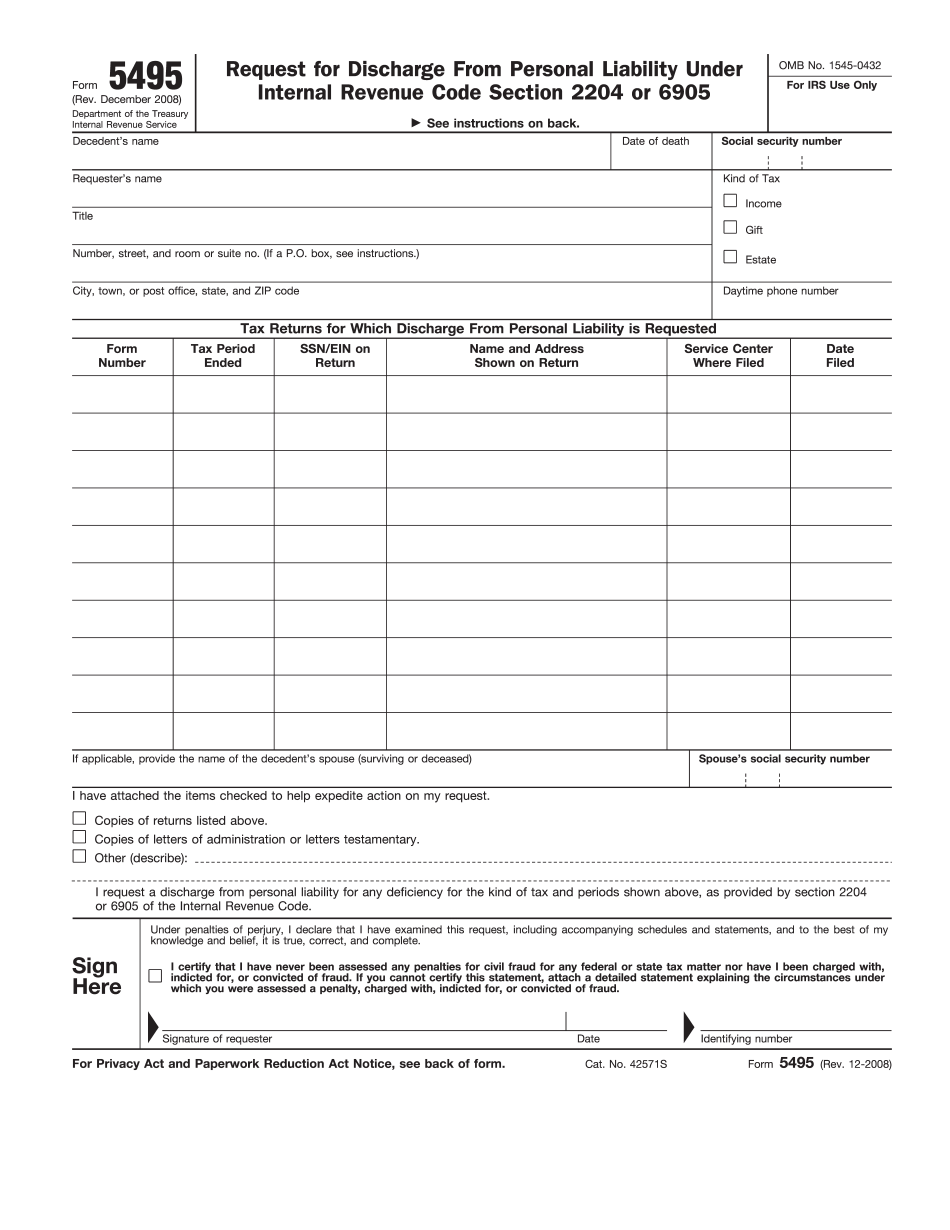

About Form 5495, Request for Discharge from Personal ... - IRS

Jun 17, 2021 — The executor representing a decedent's estate or a fiduciary of a decedent's trust file this form to request a discharge from personal ...

151161Cov G 5495 Power Module Installation Manual

Form C Trouble Relay The 5495 includes a general trouble relay that will de-energize for any trouble situation. (see Section 4.4.1 for details).

Get Form

100%

Loading, please wait

.

.

.